Key insights

- The past five years have been a master class in crisis management. We asked business leaders what decisions had helped their business survive — or even thrive — during this period.

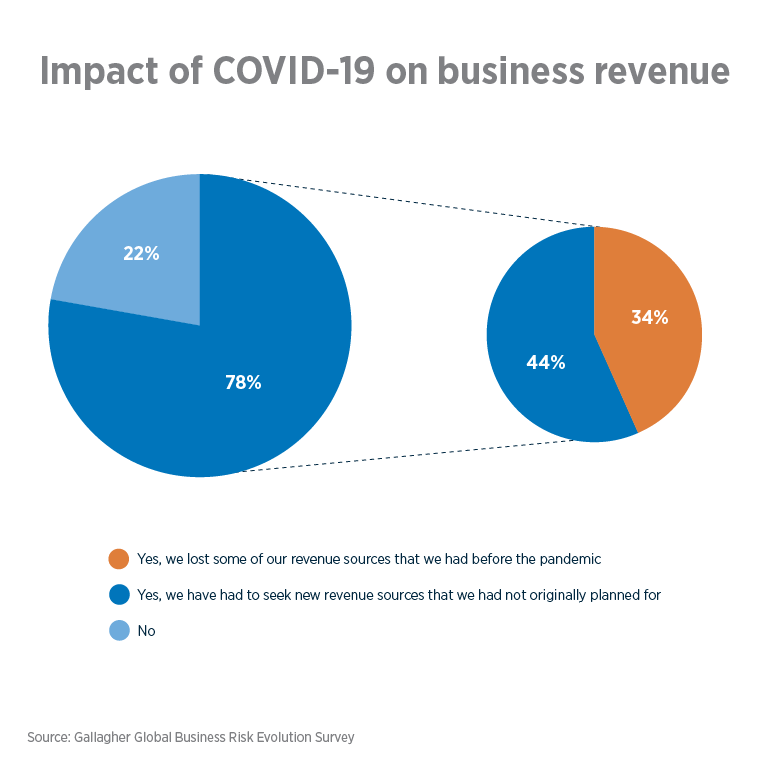

- For 78% of respondents, the volatility of the polycrisis era forced firms to seek new, unplanned revenue sources as they adapted to new circumstances.

- Notably, businesses that pursued new revenue streams were more inclined to pivot toward innovation and emerging opportunities, such as investing in technology.

- Post COVID-19, many firms have emerged with a changed risk appetite and heightened appreciation for enterprise risk management (ERM) and insurance.

- The findings paint a picture of a resilience playbook centered on strong leadership and adaptability, with a strong alignment to risk management and strategy.

The past five years have been unlike any other in modern business history — the global pandemic, geopolitical unrest, climate shocks and digital transformation have reshaped the business landscape. But they also have reshaped business leaders' relationship with risk.

After COVID-19: Five years of polycrisis

Cumulatively, the events of the past five years have been a catalyst, reshaping how organizations approach risk. Arguably, many businesses have emerged from this period better equipped for the shocks that may lie ahead. The decades old "just in time" approach to manufacturing is giving way to a more resilient "just in case" and "friend-shoring" mindset, as companies adjust to a more fragmented global economy.

To explore how companies are responding to a "permacrisis" world, we tracked the journey of the past five years through the lens of 1,200 business leaders. Our research shines a light on some of the defining traits of resilient companies and the risk appetite of business leaders, who overall say they are feeling more prepared for today's uncertainty than they were before COVID-19.

"This situation also presents an opportunity to approach challenges differently. In 2020, many were forced to adapt, leading to diversification. Faced with a catastrophic environment, people took on business risk management as a necessity for survival. This realization — that opportunities can arise from negative circumstances — is now more widely accepted."

The pandemic era: "Just in time" becomes "just in case"

For most companies, the volatilities of the COVID-19 era — marked by country lockdowns, supply chain disruptions and equity market volatility — ushered in a fundamental shift in their revenue makeup.

Note: The chart on the right represents the 78% of respondents who answered 'yes.'

In total, 78% of the business leaders surveyed said their firms had to seek new sources of revenue during the pandemic. This was especially pronounced among international and dual-market firms.

Notably, businesses that pursued new revenue streams were more likely to say the level of risk in the world had increased and were more inclined to pivot toward innovation and emerging opportunities, such as entering new territories and investing in technology. Rather than buckle under pressure, many companies acted decisively during this period, adapting business models and building buffers where possible.

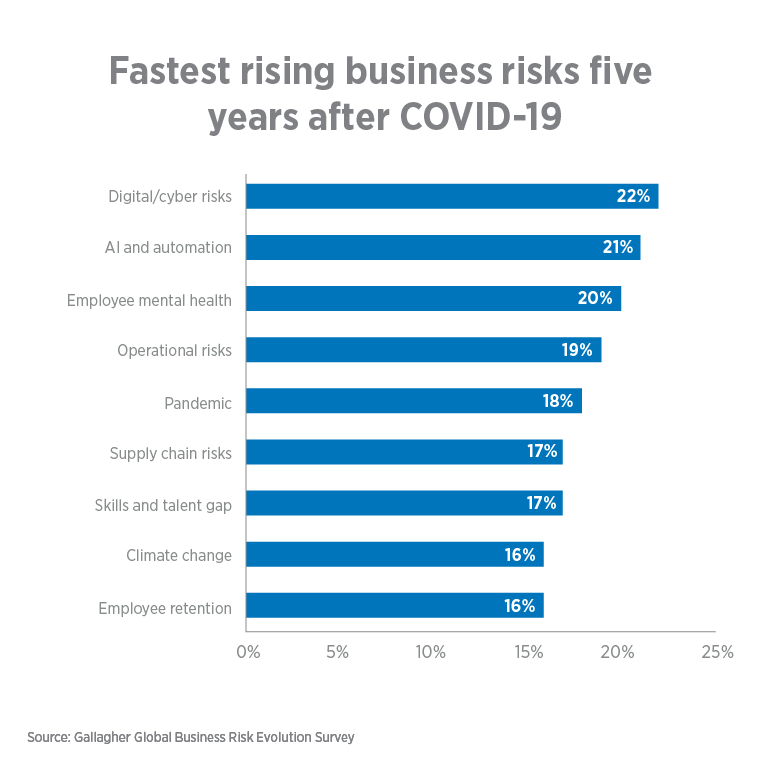

The new face of business risk: digital, operational and people

Note: Percentages are based on multiple choices per respondent.

While technology continued to drive growth in the post COVID-19 era, it also introduced emerging risks that are dominating today's threat landscape.

For 22% of business leaders, the types of business risk that have surged in priority since 2020 are cybersecurity and digital risks, followed closely by concerns around AI and automation. Despite these concerns, optimism runs high, with 96% of business leaders expressing confidence in their ability to manage these risks moving forward.

Operational risks also have surged as a top priority for 19% of businesses, spurred by economic instability, the rising cost of energy and materials and fragility of global trade to geopolitical and environmental forces.

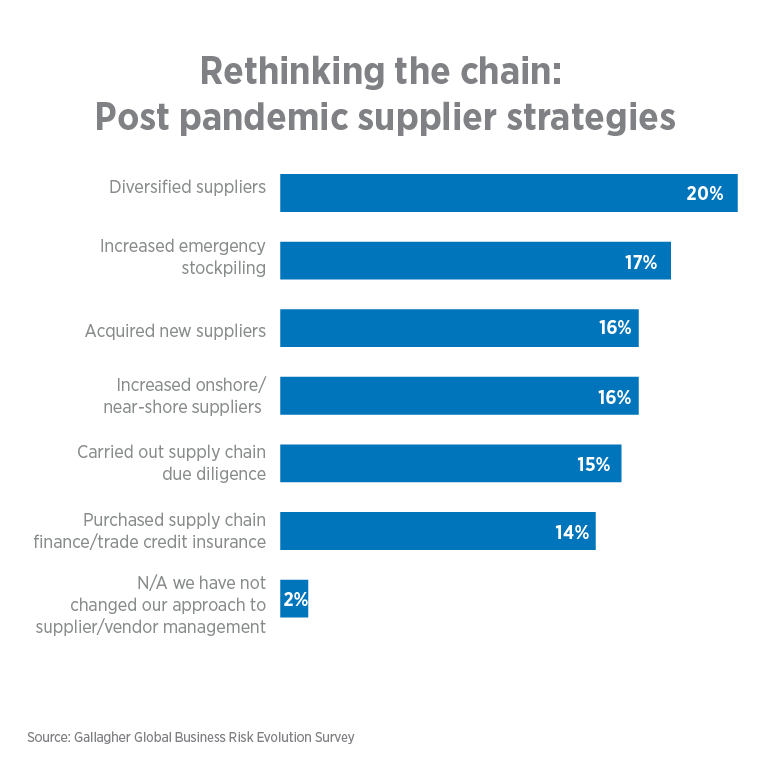

Having experienced business interruption, supply chain restrictions and the increased cost of doing business, firms have adapted by building in more contingencies. Strategies to manage supply chain risk were implemented to reduce the impact of global trade volatility. Together, they mark a shift toward smarter, more risk-aware inventory strategies.

Supplier diversification emerged as a key safety-net strategy: Over a third (37%) of business leaders say they have expanded their supplier base during the last five years, while a quarter have upped the number of onshore suppliers. One-fifth have invested in stockpiling to build some buffers into their production lines in case of an interruption.

Note: Percentages are based on multiple choices per respondent.

For employers, the COVID-19 era and rise of digital automation has prompted rapid and ongoing change within the workforce.

The impact of the pandemic on people — including health and safety fears, the shift to remote working, "Big Quit" and cost-of-living inflationary pressures — are among the factors propelling people risks up the business risk agenda.

Skills gaps and staff retention rank among the top 10 business risk management challenges for respondents, while employee mental health is considered the third most challenging risks of the past five years. The findings underscore how people risks are now just as critical as financial risks for many organizations.

Climate-related events front of mind for US business leaders

Adapting to the "new normal" — shifting attitudes to risk

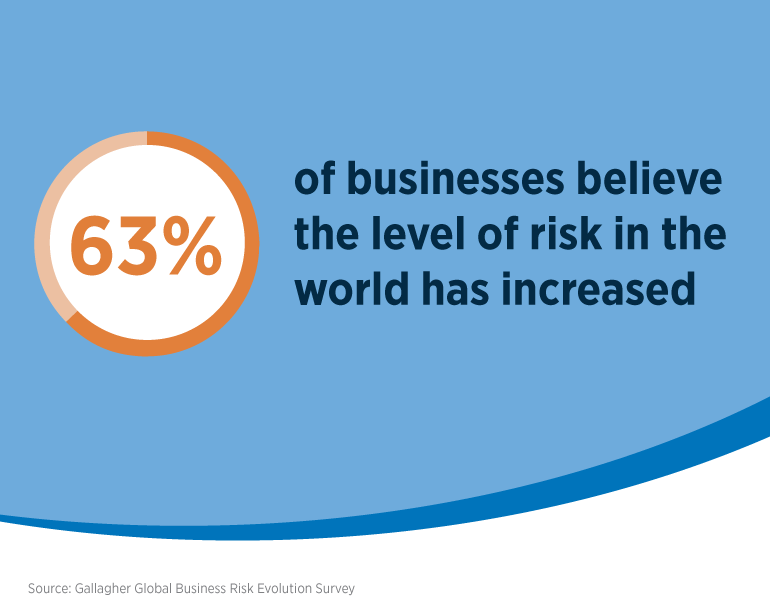

After five years of "polycrisis," most business leaders acknowledge we are operating in a riskier world. In response to this, two distinct attitudes to risk have emerged.

Some organizations — particularly larger corporations operating internationally — are more comfortable with taking on risks than they were before, and have increased their internal risk management efforts. Over half (56%) say that the risks retained within their own operations have risen during the past five years, in part driven by a more challenging commercial insurance market.

As a result, a significant majority of business leaders (81%) say they are now more risk-tolerant, driven by a clearer understanding of today's threat landscape, all-important data and insights, and a strategic push for bold, adaptive growth.

The change is most pronounced among large corporates, with 60% experiencing a change in risk appetite (both positive and negative) in the past five years, compared to smaller firms.

By contrast, business leaders who say they are more risk averse now than they were at the start of 2020 place more emphasis on the impact that COVID-19 had on the business risk landscape. They are also less likely to have prioritized leadership and recruitment to manage risk within their business over the last five years.

How have the past five years reshaped your risk mindset?

Firms appreciate risk management and insurance more than they did

A standout theme is business leaders' deeper appreciation for robust risk mitigation strategies. Nearly one in five firms have hired risk managers and added operational resilience personnel to their processes in the past five years. Three-quarters (76%) of these leaders have maintained their expanded risk functions post pandemic.

Over half of businesses with expanded risk managers and business continuity teams plan to keep them in place for at least the next five years, suggesting five years of polycrisis has elevated the role of business risk management within the organization.

Moreover, risk managers, business continuity managers and internal risk teams are considered the most trusted sources of risk insights and advice.

Business leaders report feeling more protected by their insurance than was the case five years ago. Over half have increased how much insurance they buy, while 44% say they have taken out new types of coverage.

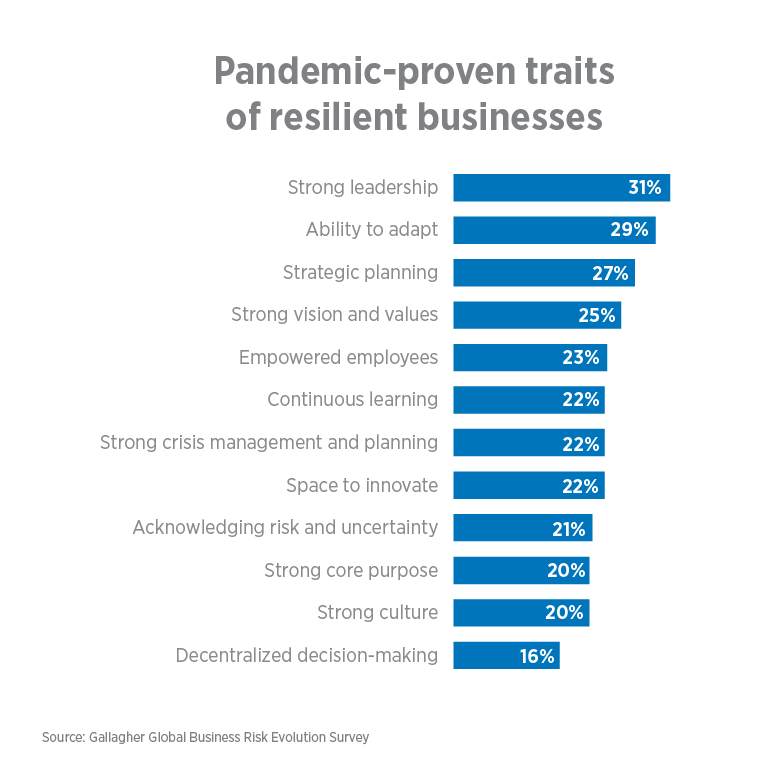

Beyond survival: A blueprint for resilience and business risk tolerance

Despite the constant slew of curveballs of the past five years, most business leaders are surprisingly upbeat, describing their business as productive, resilient and innovative.

Their resilience playbook centers on strong leadership, adaptability and strategic planning — supported by empowered teams, a strong organizational identity and proactive crisis management to weather uncertainties.

Note: Percentages are based on multiple choices per respondent.

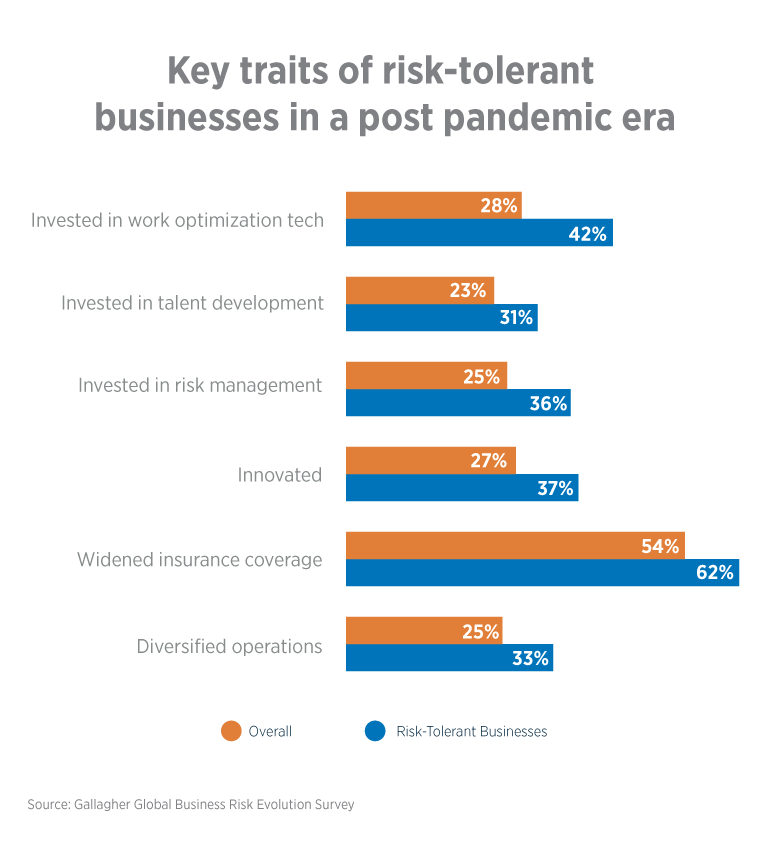

One notable shift in today's worldview is how organizations perceive — and act on — risk. Those that see themselves as more risk-tolerant credit their pandemic era gambles for helping them adapt and grow when others are more tentative.

Risk-tolerant businesses tell us they're not just embracing uncertainty, they're actively managing it. They've invested strategically in risk management — both internally via talent development, and externally by expanding their insurance coverage.

Risk-tolerant businesses also have taken deliberate steps to fuel growth over the last five years — adopting digital technology, innovating new offerings and diversifying their operations.

As one business put it, these proactive measures have given them "a clearer, more predictable view of the future moving forward, so (they) know where it is feasible to take on risk," fostering a more opportunity-led relationship with risk.

Note: Percentages are based on multiple choices per respondent.

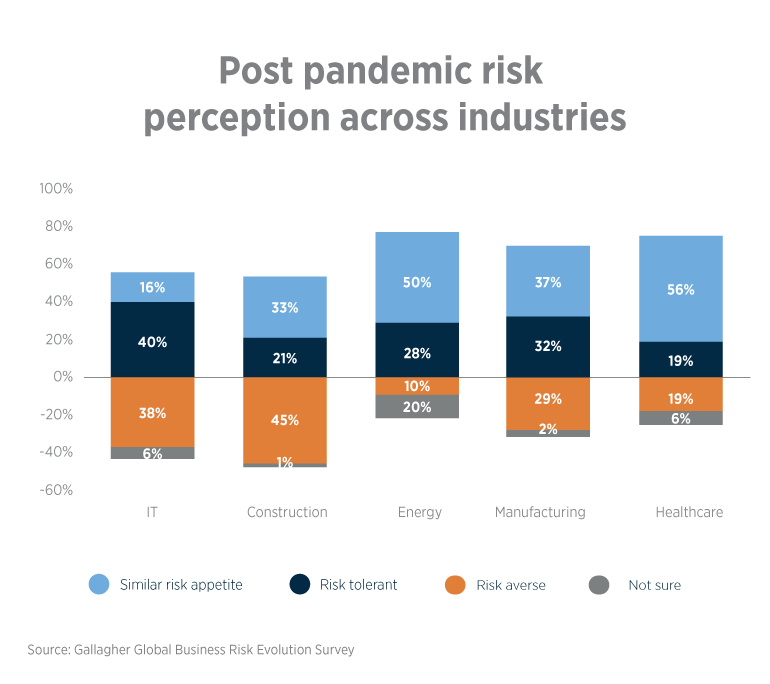

Inevitably, how shock events are experienced influences how different sectors respond. Our research findings suggest that construction, manufacturing and telecommunication now have a more polarized view of risk than they did at the start of the pandemic.

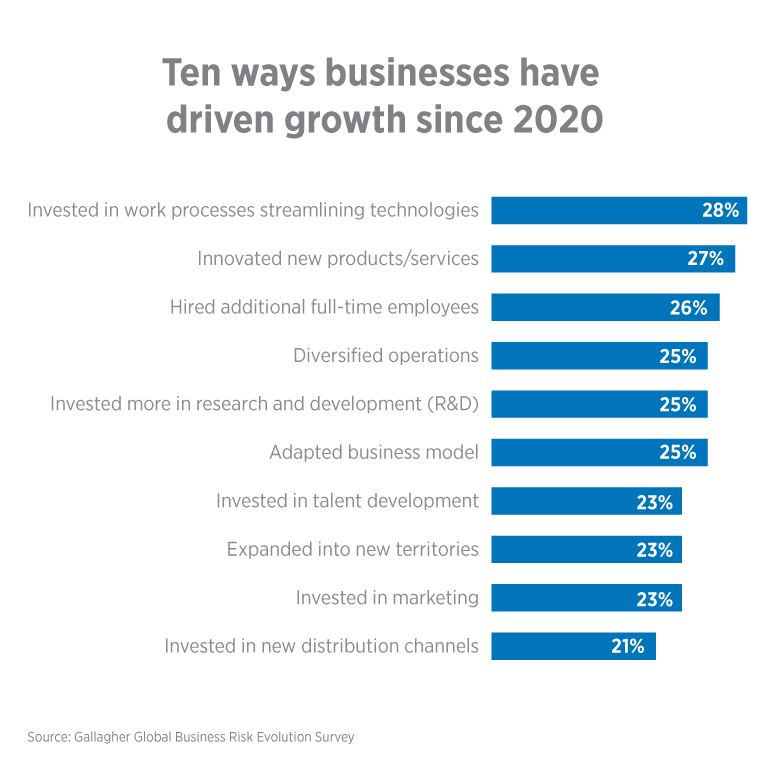

Growth and innovation take center stage

What sets resilient businesses apart from those that struggled during the crisis? The answer lies in their ability to adapt and remain nimble. In the last five years, 99% of businesses leaned into growth — leveraging technology, expanding operations and scaling up through hires, mergers and acquisitions to stay future-ready.

Interestingly, 60% also reported changes to their insurance programs as a result, reflecting the role of insurance as a facilitator of economic growth.

Note: Percentages are based on multiple choices per respondent.

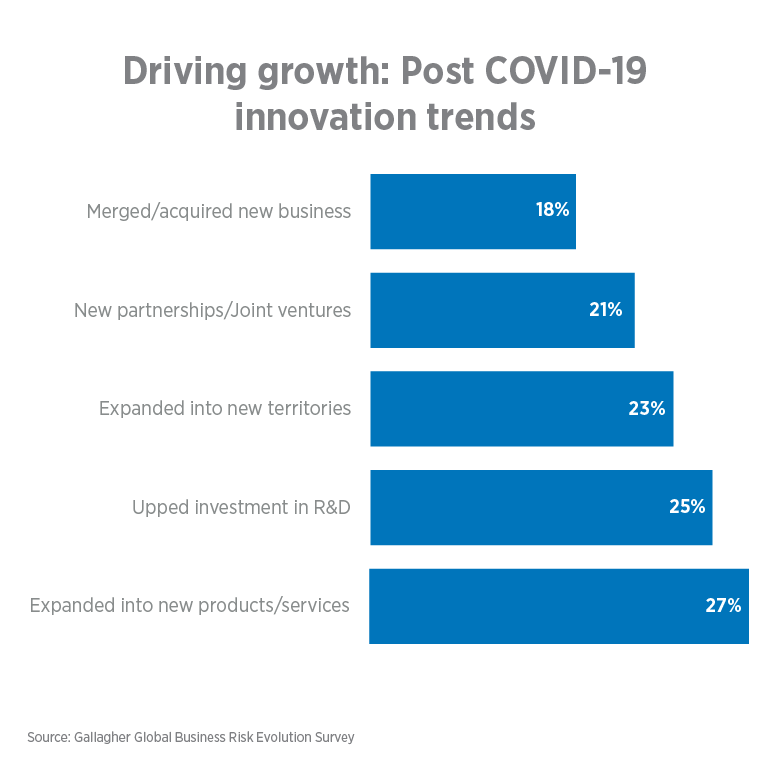

Business leaders told us they are driving growth through innovation. Once seen as a challenge, respondents now see "more benefits than drawbacks to being the first to market with a novel offering," and are pioneering new avenues to grow, backed by investments in people and R&D.

Note: Percentages are based on multiple choices per respondent.

Overall, larger firms appear more bullish than small and medium-sized firms, with business leaders from the large corporate segment experiencing higher-than-average levels of innovation.

Risk appetite also influences how firms experience innovation. Risk-averse businesses are cautious about pursuing new avenues and opportunities, as there is an "increased uncertainty about the return on innovation investment."

Risk-tolerant firms, however, see innovation as the path to productivity, agility and remaining relevant in a rapidly changing world.

Future outlook: Finding opportunity amid the turmoil

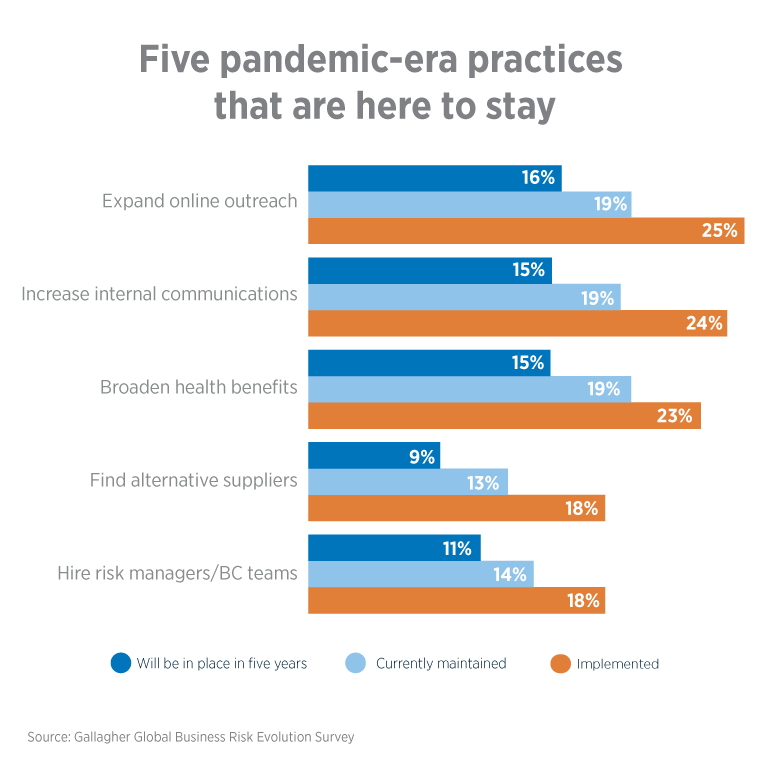

The impact of the new normal? Businesses are getting better at aligning risk perception with preparedness. While not all crisis-era changes will last, many are here to stay, including heightened crisis and risk management capabilities.

Note: Percentages are based on multiple choices per respondent.

As companies adapt to a new world, most business leaders say they feel better equipped to manage business risks now than at the start of the global pandemic. Risk is no longer seen as just a downside to avoid or mitigate, but as a facilitator of growth and innovation.

There is more recognition that risk and opportunity are two sides of the same coin, setting the stage for how businesses will respond to shocks and uncertainty moving forward.

"The pandemic affected everyone simultaneously," Hodgson says. "We understood the concept of a pandemic, but very few anticipated its global consequences. The world has come to recognize the necessity of managing risk.

"This realization — that such events can occur and affect us all — is, in my opinion, a positive development. The upside of effective risk management and risk assessment has become evident and businesses that handle risk well have adapted better to the current landscape."

Published June 2025